With just 30 days to go before the start of hurricane season, the Board of the Texas Windstorm Insurance Association (TWIA) will meet tomorrow, Friday, May 3, 2013, in Austin to discuss issues critical to its survival. Among the items on the agenda are purchases of reinsurance and attempts to sell both pre-event and post-event bonds. Both of these items are likely to prove extremely difficult for TWIA to manage. Not on the public agenda is any further consideration of having TWIA placed into receivership.

Reinsurance

Let’s look at the reinsurance issue first. TWIA will be receiving a presentation from its long time insurance broker, Guy Carpenter. You can get a copy of that presentation here. It’s a fascinating document. It rests on an awfully cheerful view of TWIA’s ability to sell post-event bonds. That’s not a view shared by the Texas Insurance Commissioner or, for what it is worth, by me. It shows TWIA is considering a reinsurance purchase option that would help insurers but would hurt policyholders. And it exposes yet again the extent to which the never-ending need to purchase reinsurance created by the undercapitalization of TWIA, forces TWIA to pay extremely high rates for that protection. If one wanted Exhibit A for why TWIA should be substantially depopulated rather than propped up so it can expand, the material for this board meeting would not be a bad place to start.

WHY IS GUY CARPENTER ASSUMING REINSURANCE CAN ATTACH AT $2.3 BILLION?

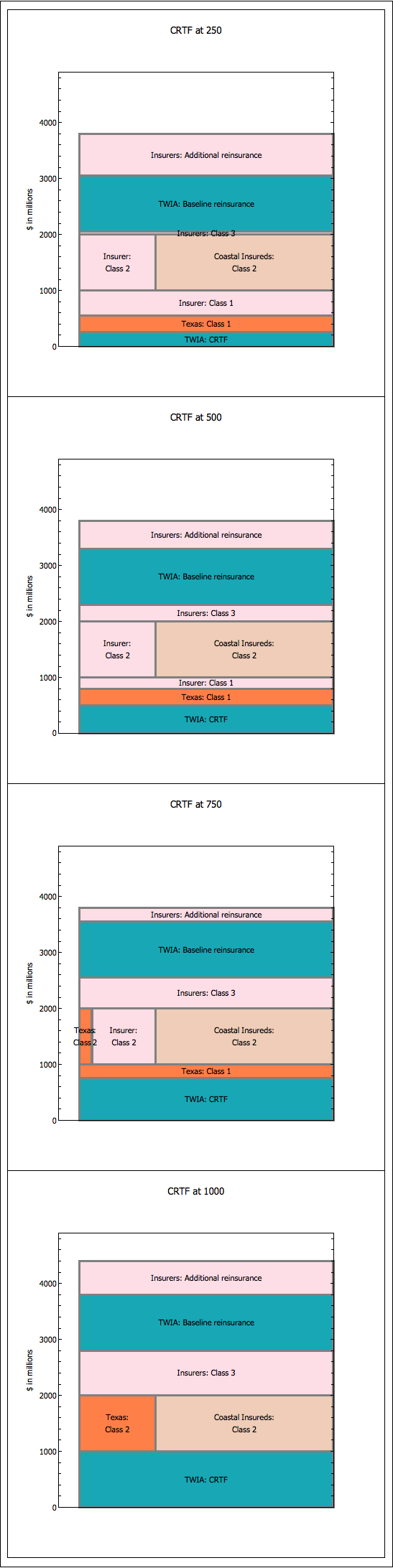

The Guy Carpenter presentation proceeds on the dubious assumption that TWIA can sell post-event bonds and thus can attach as high as $2.3 billion in the funding stack. Look at the following picture found on Slide 8. (You may need to click on it, which will cause it to zoom in).

Proposed reinsurance arrangement for 2013

Notice that it presupposes that TWIA will be able to sell $2 billion worth of Class 1, Class 2 bonds and thus explores attachment at the top of the Class 2 stack. But this is a very strange assumption to make. First, as the Texas Public Finance Authority and the Texas Insurance Commissioner have stated, and as seems clearly correct, TWIA will not be able to sell the full $1 billion of Class 1 bonds. And has been discussed on this blog before, the Class 2 bonds can’t sell if the Class 1 bonds don’t sell out and the Class 2 Alternative bonds have difficulties as well. So, the whole discussion of reinsurance attaching no lower than about $2.3 billion rests on what sure looks like unwarranted optimism.

Now, to be sure, TWIA’s got a document in its packet for the meeting Friday that suggests it still thinks it can sell $500 in pre-event securities, $1 billion in Class 2 public securities and $500 million in Class 3 securities. This document appears, however, to ignore section 2210.6136 of the Texas Insurance Code, which says that Class 2 Bonds can’t be issued unless the full $1 billion of Class 1 bonds sell out. If the Class 1 bonds don’t fully sell, then one has to resort to the Class 2 Alternative bonds. But as I’ve pointed out before, the Class 2 Alternative bonds may be almost as dubious as the Class 1 bonds. And the Class 3 bonds legally depend on all the Class 2 or Class 2 Alternative bonds selling out. So, again it looks to me as if TWIA is still looking at this summer with very rosy glasses or has some interpretation of the Texas Insurance Code I don’t understand.

Note 1: There is an alternative presentation on slide 13 in which Guy Carpenter explores the possibility of the reinsurance attaching at $1.7 billion, but even this is an awfully optimistic perspective on TWIA’s ability to sell post-event bonds.

Note 2: In fairness to Guy Carpenter, there is a footnote attached to the graph stating “Actual amounts of bond tranches are subject to marketability.” Yes. But unless there’s been some miraculous turn around in TWIA’s bonding ability, this seems like the main point, rather than a footnote.

Why is Guy Carpenter not having the reinsurance attach at the top of the Class 3 bonds?

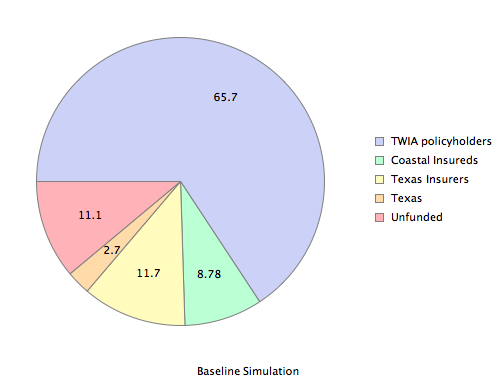

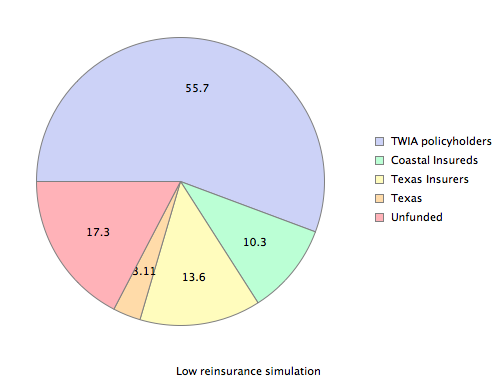

If you’ve ready my blog entry on The Curious Matter of Reinsurance Attachment, you’ll know that the TWIA board has to make a crucial tradeoff in determining where any reinsurance should attach. Inserting the reinsurance between the Class 2 and Class 3 bonds protects insurers from assessments but buys, dollar for dollar, less protection for TWIA policyholders. Inserting the reinsurance on top of the Class 3 bonds gives policyholders more protection but increases the likelihood that insurers will have to pay.

Most of the bills pending in the legislature would prohibit TWIA from doing exactly what the Guy Carpenter presentation appears to suggest: protecting insurers from having to pay back Class 3 bonds rather than maximizing policyholder protection. Given the incredibly precarious situation facing TWIA policyholders this summer — sorry insurers — but the reinsurance should attach at the highest level possible, buying the most protection for policyholders with a provision for drop down in the event the post-event bonds can’t be sold.

The pricing of reinsurance continues to be incredibly high

The Guy Carpenter proposal suggests that TWIA is again going to have to pay through the nose for reinsurance partly as a result of it never having an adequate internal catastrophe reserve trust fund. As I’ve spoken about on many occasions, this reinsurance trap — almost like borrowing from payday lenders to address financial vulnerability — basically insures that TWIA never escapes its poverty.

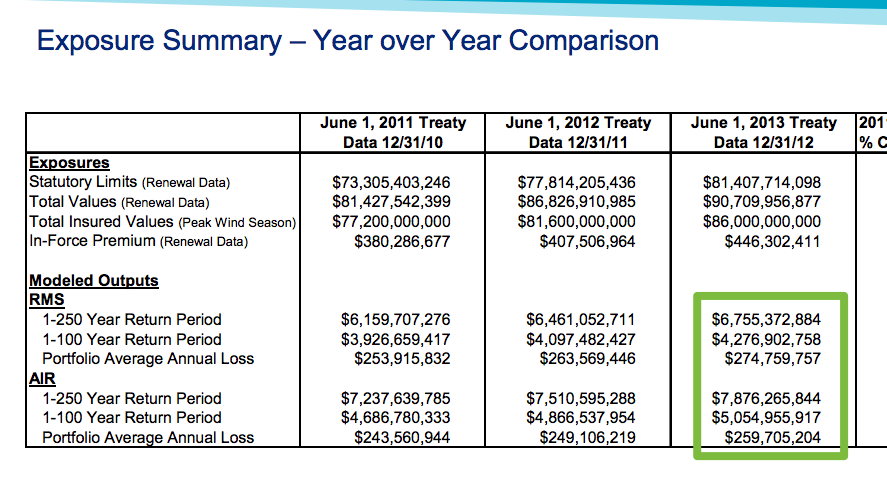

How can I say this? Look at the models AIR and RMS provide both Guy Carpenter and TWIA. Here’s slide 6 of the presentation.

AIR and RMS risk estimates

If one assumes that the distribution of annual losses is a Compound Poisson distribution, with the Poisson parameter being 0.54 (as found in this scholarly article) and one assumes that the underlying distribution is a Weibull with parameters 0.42 and 177,000,000, you can generate data that matches up extremely well with that found by AIR and RMS. If you then run, say, 10,000 years of simulations using that distribution, you find that the mean losses to an insurer who writes a maximum of $850 million worth of coverage over a $2.3 billion retention is only about $20 million. That is 4-5 times less than what the reinsurers are apparently proposing to charge. And, thus, the cost of having to reinsure rather than internally finance is something like $65-$75 million per year, or about 1/6 of all TWIA’s premiums. You dont, by the way, get qualitatively different results using the three parameter Weibull distribution that I’ve used on this blog before to replicate the AIR/RMS models.

There’s a lot more that is odd about the reinsurance pricing. If we think of the price as being composed partly of expected losses and partly of having to withdraw the maximum exposure from illiquid high-earning investments and place it in low return, highly liquid investments — this is the Wharton School model — the pricing only makes sense if reinsurers lose about 7.8% on their capital by having to make it particularly liquid. ((-expectedLosses + premiums)/maxExposure). Given the market right now, that’s a pretty high number.

There are a couple of explanations between the actual pricing for reinsurance and the pricing that the models would suggest. One, which is rather scary, is that the reinsurance market is not behaving as competitively as one would like. The other, scary for different reasons, is that the reinsurance market doesn’t trust the AIR/RMS model and thinks the risk of a major hurricane is considerably greater. If that’s true, however, then even the dire warnings that I and others have been sounding about TWIA are understated.

Bonds

The Bond Anticipation Note

The other main item on the agenda appears to be the issuance of bonds. There is a a proposal from First Southwest that TWIA sell by June 27, 2013, a “Bond Anticipation Note” for $500 million that would basically be an advance on a hoped-for similar Class 1 post-event bond. First Southwest apparently believes these unrated bonds could be sold at between 4 and 6%. My own 2 cents is that if TWIA can get this loan, it should grab it. Increasing the amount it has to pay claims from its CRTF funds of $180 million to something like $680 million will help. And if all it has to pay is some interest, that’s a good deal. But there’s a lot to do before this money will be available to TWIA and it looks as if it is going to have go through at least the first month of the 2013 hurricane season without it.

Post-Event Bonds

There’s also apparently a resolution on the table authorizing TWIA to asks the Texas Public Finance Authority to issue post-event bonds. I’ll confess I don’t understand this one. There haven’t been any tropical cyclones yet in Texas for 2013. Maybe TWIA is getting this resolution done to see what can actually done for 2013? Maybe it is an attempt to see if things are as bad as some people have been saying?

Conclusion

The TWIA board is in a very tough spot. With fewer than 30 days to go in the legislative session and 30 days until the start of hurricane season, it doesn’t really know what its resources are to pay claims. It’s being (understandably) threatened with receivership by the Texas Insurance Commissioner. And its existing reinsurance expires on May 31, 2013, before the start of hurricane season. If and until TWIA gets some legislative relief or is put partly out of its misery by a Texas shift to an assigned risk plan or other mechanism that deconcentrates risk, it doesn’t have many good options. My hope is that the board will have the courage to confront its moral and legal obligation to warn policyholders in the clearest possible terms of the risks that, unless powerful legislative relief swiftly occurs, their claims will not be paid fully should a significant hurricane hit this summer.