The short term finances of the already shaky largest property insurer on the Texas coast took an unanticipated and significant turn for the worse Monday. Outgoing Texas Insurance Commissioner Eleanor Kitzman rejected Monday plans of the Texas Windstorm Insurance Association to borrow $500 million via a “Bond Anticipation Note” to help pay claims this hurricane season. The Commissioner did not reject a plan to issue post-event bonds in the event of a significant storm this season. As a practical matter, however, it may be difficult to persuade the market to loan money to TWIA after a storm due to peculiarities in the existing law that were not ironed out during the regular session of the Texas legislature.

The refusal to permit TWIA to borrow at this time, coupled with the announced $135 million settlement earlier this week of most of the remaining lawsuits against TWIA arising out of Hurricane Ike, probably cuts in half the amount of cash TWIA would have immediately available to pay claims in the event of a storm this summer without having to rely on untested, legally questionable and potentially slow efforts at “post-event” borrowings. The action leaves both the cash position and the long run finances of the troubled insurer in question.

My best guess is that without the Bond Anticipation Note (BAN), and including its Catastrophe Reserve Trust Fund (CRTF), TWIA probably has between $400 to $700 million in cash with which to pay claims. That’s not much when your direct exposure is over $75 billion, your total exposure is over $80 billion and a Category 2 or 3 hit at a bad spot on the Texas coast could easily cause losses of over $2 billion. The Bond Anticipation Note would have doubled the amount of cash available to pay claims.

As it stands, and as set forth below, I now believe it is not unduly pessimistic to set the odds of a TWIA insolvency this summer at 10%. If we consider two summers until the next regular legislative session, this risk roughly doubles. Given the grave effects of a TWIA insolvency on the entire Texas economy, this is way, way too high a risk.

Cash position

To understand this, take a look a TWIA’s 2012 Annual Statement. TWIA ended 2013 with about $430 million in cash (Assets, line 5; column 1) and total admitted assets (including the cash) of about the same amount, $430 million. (Assets, line 28, column 3) It has agreed to pay about $135 million in cash to settle the bulk of the Ike lawsuits. How much that will reduce the $323 million in loss reserves (Liabilities, Surplus and Other Funds, line 1, column 1) is unclear. Because lawsuits remain, it is unlikely to reduce those reserves down to zero. It will, however, likely reduce TWIA’s cash position by the full $135 million in relatively short order, depending on the details of the settlement. That would leave TWIA with just $295 million in cash.

Of course, it’s a little more complicated. I don’t have access to TWIA’s financial statements for the first quarter of 2013 or thereafter. TWIA has likely earned some cash since January 1, 2013. It has been earning and collecting premiums, although it has had to pay off about $50 million on a thunderstorm in Hitchcock. So, let’s be generous and credit TWIA with about $120 million more in new cash. This brings a guesstimate of its cash levels back up to around $415 million.

The problem is that not all of this cash is available to pay policyholder claims. Some of it will be used to pay for operations, for commissions, and for other matters, including the Ike claims not resolved earlier this week. So, I would be surprised if someone were to audit TWIA today and found it had more than $400 million in cash available to pay claims before resort to the CRTF. I would not be surprised if the number actually came out in the $300 million range. And both of these figures will be reduced by $100 million or so less if TWIA succeeds in its plan to purchase reinsurance.

So, without the hoped-for borrowings, TWIA might have had $300 million to pay claims out of operating funds and another $180 million out of its CRTF. TWIA might have had a total of $500 million. (If the settlement came out of the CRTF rather than operations, the total would stay the same). If the BAN had been approved, at least in the short run before TWIA had to pay the loan back, TWIA might have had $1 billion. Both sums are, of course, grossly inadequate to deal with the $80 plus billion in TWIA exposure. Nonetheless, $1 billion in cash would have left TWIA in a better short run position.

Long run finances

Perhaps the greater impact, however, of the BAN ban is on the ability of TWIA to sell post-event bonds following a storm. We’ve been through this matter before on this blog, but it is worth repeating because it is so very important. The short version is, however, that there is a significant risk that very little in post-event bonds will actually be able to be sold. And, thus, TWIA may very well have less than $1 billion with which to pay claims even after borrowing. I would not be surprised if it ended up with as little $700 million. The probability of such losses occurring this summer would be about 7-9% if this were a normal hurricane season. If, as climate experts agree, however, this proves to be a bad hurricane season the probability of TWIA going broke and unable to pay claims fully could rise to 10-14%.

Here’s the longer version. I, by the way, am not alone in my alarm on this matter. TWIA itself raised the issue in its submission to the Texas legislature. the Texas Public Finance Authority (TPFA) had trouble last year trying to help TWIA borrow. And several of the pieces of proposed legislation this session would have fixed this particular problem. But all of these bills failed during the regular session. Governor Perry has thus far resisted calls that he add windstorm insurance reform to the agenda for a special legislative session.

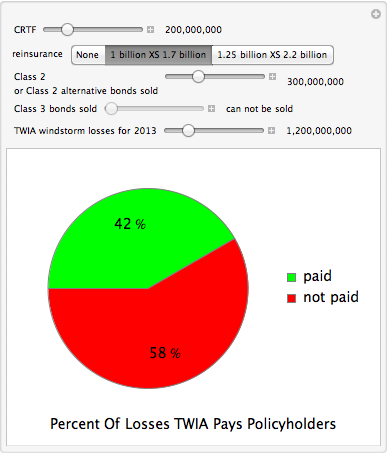

if there is a storm that pierces the CRTF, TWIA will need to rely on post-event Class 1 bonds. But, unless something has changed, per the Texas Public Finance Authority they won’t sell, at least not up to $1 billion authorized. But if the Class 1’s don’t fully sell, then TWIA/TPFA is prohibited from selling the regular Class 2 bonds. (Section 2210.073). Instead, we go to the Class 2 Alternatives under section 2210.6136. But if less than $500 million of Class 1 bonds have sold — which is likely to be the case — the first $500 million of the Class 2 bonds are paid in the same problematic way as the Class 1 bonds (surcharges on TWIA policyholders). (Section 2210.6136(b)(1)). And there is a serious question as to whether anyone will loan TWIA money on those terms. Why? Because as soon as substantial policy surcharges are issued on TWIA policies, some TWIA policyholders will either find other insurance, reduce the sizes of their policy, or simply choose to go bare. This is particularly likely if a storm has impoverished many TWIA policyholders. And if enough TWIA policyholders reduce their premiums, the percent surcharge will need to go up to compensate in order to pay off the bonds. But if the surcharge rate goes up, more TWIA policyholders will drop out. And, we get into a death spiral.

But here’s the catch. Under section 2210.6136(c), if TWIA/TPFA can’t sell every dollar of the $1 billion in Class 2 Alternatives, then TWIA/TPFA can not issue the class 3 bonds of $500 million. The statute is crystal clear on this point. And this means that TWIA has no Class 1 bonds, no Class 2 bonds, little or no Class 2 Alternative bonds and no Class 3 bonds. The system has completely collapsed in a cascade of failures. TWIA basically has no money beyond cash on hand, and the CRTF. That means policyholders will not be paid in full. If the storm is bad enough, they won’t be paid even half of their legitimate claims.

Reinsurance — assuming that TWIA can get it — will not help a lot. The reinsurance will not kick in until losses exceed the “reinsurance attachment point.” But the reinsurance attachment point is likely to be set on the false assumption that the post-event securities will succeed. So, for losses less than the reinsurance attachment point, the reinsurance won’t pay at all. TWIA will be just as bankrupt as if it did not have reinsurance at all. Actually, it will be more bankrupt because it will have paid $100 million in premiums. And even if the storm is so bad that the reinsurance kicks in, there is still a gap between the top of the CRTF plus any post-event bonds and the reinsurance attachment point. So, TWIA won’t have enough money to pay claims fully.

Why would Commissioner Kitzman do such a thing?

I’m not privy to her reasoning or all the facts, but there are concerns we have outlined before about pre-event borrowing such as a Bond Anticipation Note. The problem with loans is that you have to pay them back — and at interest. Thus, in the long run, particularly if interest rates rise or if TWIA is deemed high risk and thus charged high rates even now, borrowing perpetuates your insufficient capitalization. Whatever the benefits in the short run — and there may have been many here that incoming Commissioner Julia Rathgeber will want to examine — it is not the ideal long run solution for insurance risk. It may well be that Commissioner Kitzman refused as her final act to be complicit in the bandaiding of TWIA in the hopes that a sufficiently obvious problem would spur the Governor to call a special session and the legislature to develop a sustainable fix. If so, let us hope that gamble proves correct.