While fantasies may have their place in literature or otherwise, they are an unhealthy basis on which to premise legislative hearings. By distracting legislators from the real work that needs to be done before the end of session and providing false hope to constituents who need to take real action before the start of hurricane season, they are at least as destructive as any hurricane. That’s why the Corpus Christi Caller’s account this morning of yesterday’s meeting of the Texas Senate Committee on Business and Commerce should profoundly disturb residents of the Texas coast who depend on a viable windstorm insurance system. It should equally disturb those throughout the State of Texas whose fates are intertwined with their coastal friends. The meeting unfortunately perpetuates the absurdities of the meeting of the Texas Windstorm Insurance Association board that took place on Monday in which false villains were created and the very legislators who voted for the scheme that contributes to the current deplorable state of coastal windstorm insurance attempt through distraction to escape accountability.

Let’s identify the distracting fantasies.

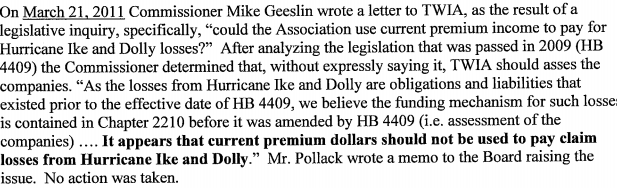

Fantasy 1. TWIA can escape insolvency by assessing Texas insurers in 2013 for Hurricane Ike.

We’ve been through this before on this blog but let’s do it again now that we have an idea of the opposing arguments. The statute authorizing TWIA to assess insurers under former section 2210.058 of the insurance code was repealed in 2009 by section 44(2) of HB 4409. I’ll reprint that statute at the bottom of this post so you can see for yourself. Government can’t just take people or business’ property for the purpose of enriching others, no matter how worthy the cause, based on a repealed statute. That’s called tyranny, and it is a violation of, among other things, the same Fifth Amendment protections that prevents the state from taking your house away to pay for worthy state expenditures and the same section 17 of the Bill of Rights contained in the Texas Constitution in which our state’s belief in those same principles is enshrined.

Until Monday, I had not heard a single argument opposed to the proposition that section 2210.058 no longer justified assessments against insurers. And, until I heard the contrary arguments, I was not prepared to say with 100 percent certainty that I was correct. But in light of a letter from several state representatives submitted to the TWIA board and made public Monday and in light of Representative Eiland’s reported comments at the hearing yesterday, we now appear to know the arguments of those who would contradict this apparently evident proposition. All I can say is, “that’s your best shot?” Here’s what they are apparently saying. If there are other arguments that I am missing, bring them on.

Argument 1: The potential to assess insurers is an “obligation, or liability previously acquired, accrued, accorded, or incurred under [a repealed statute] and is thus saved from repeal by section 311.031 of the Texas Government Code.” This argument misunderstands the nature of an obligation and a liability. An obligation or liability refers to something already existing. Thus, if State Farm did not pay an assessment already imposed prior to the repeal, HB 4409 did not eliminate the already existing powers to force State Farm to pay. But at the time when the repeal took effect, there was no “obligation,” there was no “liability” to pay an assessment based on Hurricane Ike beyond the $430 million the TWIA board did assess in 2008. The fact that TWIA might have made an assessment is no more an “obligation” or a “liability” than a tax that the legislature might have but did not impose or a penalty that a court might have but did not impose.

Argument 2: There is some sort of contractual right on the part of 2008 policyholders to an assessment. I teach contracts and I like creative arguments. But there is no such contractual right. I’ve looked at TWIA contracts and there is absolutely nothing in those contracts creating a right to an assessment. Zero. Would a Texas legislator please show the public a TWIA contract containing a right to an assessment.

It is particularly galling, I might add, to contend, as Representative Eiland apparently did at the hearing yesterday, that TWIA policyholders deserve such a right (even if they don’t actually have one?) because of the premium they paid. In fact, precisely because of actions by legislators such as Craig Eiland,TWIA policyholders were not asked to pay a premium that would permit their insurer to be capitalized adequately and that might have provided better protection against hurricanes such as Ike. Instead, those legislators forced TWIA policyholders to become dependent on the TWIA board — a politically constituted body significantly chosen from the insurance industry — exercising their discretion to assess Texas insurers adequately in the event of a major storm.

Now, it may (or may not) be that the TWIA board breached some sort of duty to policyholders by failing to assess. A letter sent by coastal legislators earlier this week contains a disturbing account of board inaction. Unfortunately, however, the choice not to include a right to an assessment in the contract takes the matter out of contract claims against TWIA itself and put it into the murky area of fiduciary duty claims against TWIA board members. And, with fiduciary duty rather than contract providing the source of rights, the remedies become far more limited. Yes, you can sue a board member for breach of fiduciary duty, but section 2210.106 of the Insurance Code promised those board members immunity from suit unless one can show bad faith, intentional misconduct, or gross negligence. And even if you get over this qualified immunity hurdle, I doubt there are too many board members who have $400 million lying around, the additional amount that TWIA officials recommended be assessed to pay for Ike.

Fantasy 2. Going into receivership would make it harder for TWIA to borrow money either before a hurricane or after a hurricane.

A lot of people at the TWIA board meeting Monday testified about the terrible problems that would be created if TWIA were thrown into receivership: sending the wrong signals, threatening continued development, threatening mortgage covenants, and threatening the Texas economy (even national security) by challenging energy production on the Eagle Ford Shale. Unfortunately, these people have confused treatment with either symptoms or disease. It is fine to be angry about cancer, but anger at being treated for cancer after a positive test comes back is misplaced indeed. And it’s insolvency here that is causing the problems and that is going to cause more problems. Receivership is a treatment for the disease of insolvency (here a disease caused by a combination of legislative dysfunction, human greed and fallibility, and a Category 2 hurricane that hit in a particularly vulnerable spot). In fact, although perhaps the matter could be deferred for a week or two to get plans in order, receivership makes a lot of sense. It would likely, as Representative Taylor appears to recognize, actually help most TWIA policyholders.

Here’s why.

Reason 1: Without receivership, there will be even less money available to pay claims for any hurricanes that hit this season. TWIA is being picked apart by claims for Hurricane Ike that are still pending. Projections are that, even if no serious hurricane hits, TWIA will have even less money by the time the year ends. Thus, if Tropical Storm Barry or Hurricane Rebekah hits this season, there is going to be even less money around to pay the new claimants. This is particularly true, if, as many fear, the recapitalization structure envisioned by the current Texas Insurance Code, is not going to work and if one of the bills pending in the legislature continues not to address issues for 2013. Those whose houses are decimated this summer by a storm are very much going to wish that someone through TWIA into receivership this spring so that 2008 policyholders and 2013 policyholders were treated more equally. So equity among TWIA claimants is one good reason for a receivership.

Reason 2: The recapitalization structure envisioned by the current Insurance Code may well be more likely to work with a receivership than without one. Someone who lends money to TWIA now has to be concerned that their claims will be paid out of the same pot as Ike claimants or other TWIA creditors. Given TWIA’s insolvency, that is worrying. It’s likely to cause lenders to demand a particularly high rate of interest if they are willing to lend at all. Although I am not certain of this, if Texas receivership is like federal bankruptcy, post-receivership financing even in a rehabilitation case can be separated out and given a higher priority that other claims. That appears to be true in Texas insurance liquidation (section 443.154(j)) and I would be surprised if it were not true in a rehabilitation as well. Now, if the rehabilitation failed, such a refinancing might hurt existing (Ike) claimants of TWIA, and one can see how they might oppose a cavalier refinance on that basis, but if one wants to give TWIA some hope or making it through another hurricane season, giving new lenders some additional protection makes a lot of sense. I don’t see how that can be done absent a receivership.

Reason 3: The parade of horribles brought forth by representatives of the coast at the hearing Monday was mostly about the problems created by insolvency, not by receivership. Mortgage companies who have imposed covenants to maintain insurance on their borrowers don’t care as much about whether the insurer is in receivership as whether that insurer has enough money to pay claims that threaten their collateral. And, yes, workers in the Eagle Ford Shale and elsewhere will be hurt if their windstorm insurance premiums go up and their corporate employers don’t respond with higher wages, but what happens to premiums is not particularly dependent on a receivership. It is dependent on an understanding of why TWIA went insolvent and the proposals pending in Austin to reform TWIA.

At best, the argument against receivership is thatTWIA, a so-called “residual market” carrier, was not really “insolvent” in the same way a private insurer would be if its liabilities exceeded its assets. That’s because, this point proceeds, TWIA has a statutory right to recapitalize through assessment and surcharge that other insurers do not following a major disaster. So, it is true that, at least for a while TWIA will be able to pay its bills. But inability to pay bills is not and should not be the only basis to justify a receivership. Another reason is equal treatment of claimants. The recapitalization mechanism was never very solid and is now so dubious that there is a serious question whether TWIA can treat current policyholders fairly.

Fantasy 3: Resolutions of the receivership issue and assessment issue are very important.

Receivership is an issue, but it is not the main issue. It will just determine at the margin how current and future TWIA claimants get paid and may have some effect on solvency this summer. Even an assessment of another $400 million or $500 million to fully pay for Ike, though it would help current TWIA claimants, will do little to fix the most fundamental problems with that entity, which include its perpetual undercapitalization and the instability and unfairness of its funding mechanisms. Even with an assessment and with or without a receivership, the current law means that TWIA is running a very substantial risk of going insolvent this year from another serious storm. Or, in plain English, if you own property on the coast and it is hit by a tropical cyclone this summer, there is a troubling chance TWIA will not actually be able to pay what it owes you and you may have trouble rebuilding.

The main issue is how to address windstorm insurance on the coast both for the coming hurricane season and thereafter. There are two serious proposals before the legislature. One basically proposes depopulating TWIA and moving toward a market-based system backstopped by an assigned risk plan for those areas in which the market fails to provide insurance close to some affordability threshhold. Under this system, although people across Texas very definitely help, coastal policyholders bare most the burden of the risk posed to their property. Coastal propertyholders get the benefits of owning real estate near the Texas coast, but they also pay for it. The second proposal continues to force people — poor people and rich people alike, Amarillo residents, El Paso residents and Nacogdoches residents — to subsidize risk along the coast even more than has been done before. While this system at least reduces the risk of a hurricane leaving insureds with claims only against an insolvent insurer, it sends bad signals to the development market and, gallingly, frequently transfers money from the poor to the wealthy. I have my own views on how that debate should come out but respect the view of others. I just wish it was that debate that was preoccupying the Texas legislature and not a judicial remedy for addressing the existing insolvency.

Here’s what Representative Craig Eiland reportedly said yesterday:

“I see no way you could ever say that’s there no assessment authority with TWIA based on the contractual rights the 2008 policyholders have for the premium they paid for the coverage they purchased,” he said. “Why are we dancing around the question? If we go into receivership the judge is going to assess the companies and have an answer. Why are we not trying to have an answer? Before you make the decision that we cannot assess, how about go assess and find out the final answer.”

Text of section 44 of HB 4409 (found here)

| SECTION 44. The following laws are repealed: | ||

| (1) Subdivisions (5) and (12), Section 2210.003, | ||

| Insurance Code; | ||

| (2) Sections 2210.058 and 2210.059, Insurance Code; | ||

| (3) Sections 2210.205 and 2210.206, Insurance Code; | ||

| (4) Sections 2210.356, 2210.360, and 2210.363, | ||

| Insurance Code; and | ||

| (6) Subchapter G, Chapter 2210, Insurance Code. | ||