According to newspaper accounts here and here, S.B. 1700 is heading for a vote in the Texas Senate this week. Before the Senate votes on the bill or the House Insurance Committee considers the matter, I hope they have some understanding of how radically it transfers wealth to TWIA/TRIP policyholders from people who do not have TWIA policies. I also hope legislators understand that although a $4 billion funding stack is definitely an improvement over the status quo, there is still a significant risk to the coast. And I also hope they understand the TWIA/TRIP depopulation plan, which would in theory be a good idea, has about as much a chance of success without giant changes to TWIA and TRIP that will greatly anger coastal residents as a plan to depopulate Texas itself.

Here are some pictures that I hope aid understanding.

The Funding Stack

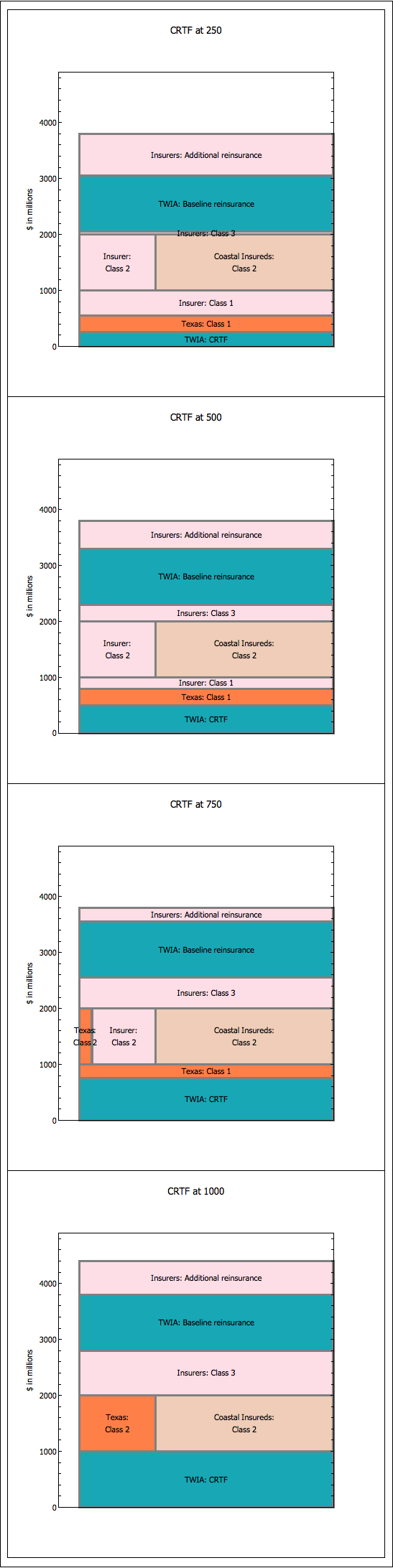

Here’s a picture of the TWIA funding stack for 2013 under S.B. 1700. For each element of the stack, I’ve shown who actually pays for that layer of responsibility.

![SB 1700; Labeled[BarChart[{180, 500, 500, 500, 500, 1000, 800}, ChartLayout -> "Stacked", ChartLabels -> Placed[{"Catastrophe Reserve Trust Fund (TWIA premiums)", "Class 1 Assessments (Texas insureds)", "Class 1 Securities (Coastal insured surchanges)", "Class 2 Assessments (Texas insureds)", "Class 2 Securities (Coastal insured surcharges)", "Baseline Reinsurance (TWIA premiums)", "Insurer Purchased Reinsurance (Texas insureds)"}, Center], BaseStyle -> {FontSize -> 11, FontFamily -> "Swiss", LineIndent -> 0}, ChartStyle -> Map[Lighter@ColorData[61][#] &, Range[8]]], Style["TWIA Funding Stack for 2013\n(Numbers in Millions)", \ {FontSize -> 11, FontFamily -> "Swiss", LineIndent -> 0}]]](http://catrisk.net/wp-content/uploads/2013/05/FundingStackSB1700.png)

TWIA Funding Stack for 2013 under SB 1700

Distribution of expected responsibility

Here’s a pie chart based on a 10,000 year storm simulation showing how much each layer of responsibility would expect to pay under S.B. 1700. There are several features of this graph worth noting. First, note that TWIA policyholders have paid only for the modest dark red wedge at the left and the orange baseline reinsurance at the bottom left. That is less than half of the expected payments. (Yes, they pay a modest portion of the coastal insured surcharges too, but we don’t know how much). Also notice the large cherry red wedge of unfunded losses. Although the stack goes up to $4 billion or so under this bill for 2013, and although insolvency now occurs in perhaps 1.5% of the years (26% over 20 years), when insolvency occurs, it is a huge amount of money that is unfunded.

By Layer

![SB1700; Framed@Labeled[PieChart[Mean /@ Through[funcs[rv]], ChartLabels -> Placed[Map[ Pane[#, 144] &, {"Catastrophe Reserve Trust Fund and operating \ funds (TWIA premiums)", "Class 1 Assessments (Texas insureds)", "Class 1 Securities (Coastal insured surchanges)", "Class 2 Assessments (Texas insureds)", "Class 2 Securities (Coastal insured surcharges)", "Baseline Reinsurance (TWIA premiums)", "Insurer Purchased Reinsurance (Texas insureds)", "Unfunded losses"}], "RadialCallout"], ChartLegends -> Placed[{"Catastrophe Reserve Trust Fund and operating funds (TWIA \ premiums)", "Class 1 Assessments (Texas insureds)", "Class 1 Securities (Coastal insured surchanges)", "Class 2 Assessments (Texas insureds)", "Class 2 Securities (Coastal insured surcharges)", "Baseline Reinsurance (TWIA premiums)", "Insurer Purchased Reinsurance (Texas insureds)", "Unfunded losses"}, Bottom], ChartStyle -> Map[ColorData[61][#] &, Range[8]], ImageSize -> 580, ImagePadding -> {{90, 100}, {20, 20}}, BaseStyle -> {FontSize -> 11, FontFamily -> "Swiss"} ], Style[ "Distribution of expected loss payments by layer", {FontSize -> 14, FontFamily -> "Swiss", FontWeight -> Bold}] ]](http://catrisk.net/wp-content/uploads/2013/05/SB1700responsibilityByLayer.png)

Expected loss payments by layer based on 2013 stack

By source

We can group the expected payments shown above so that we simply have expected payments by source. Here is that graph. Notice again that TWIA policyholders pay little more under this scheme than either Texas insurers (who will surely pass the cost on to non-coastal Texas insureds) and coastal insureds, many of whom have already paid for non-TWIA wind policies. And, again, notice the large chunk of unfunded losses that exists under S.B. 1700.

![With[{wedges = With[{t = {#[[1]] + #[[6]], #[[2]] + #[[4]] + #[[7]], #[[3]] + \ #[[5]], #[[8]]} &[Mean /@ Through[funcs[rv]]]}, t/Total[t]]}, Framed@Labeled[ PieChart[wedges, ChartLabels -> Placed[Map[ Pane[#, 144] &, {"TWIA premiums", "Texas insurers (insureds)", "Coastal insureds", "Unfunded losses"}], "RadialCallout"], ChartStyle -> Map[ColorData[61][#] &, Range[4]], ImageSize -> 580, ImagePadding -> {{90, 100}, {20, 20}}, BaseStyle -> {FontSize -> 11, FontFamily -> "Swiss"} ], Style[ "Distribution of expected loss payments by layer responsibility", \ {FontSize -> 14, FontFamily -> "Swiss", FontWeight -> Bold}]] ]](http://catrisk.net/wp-content/uploads/2013/05/SB1700responsibilityBySource.png)

Distribution of expected loss payments by layer responsibility under SB 1700

By Cash Payments

There’s another way to look at S.B. 1700. Don’t focus on the source of expected loss payments. Focus instead on source of expected cash flow. The two are not the same because large chunks of cash flow get lost in TWIA/TRIP overhead and in paying reinsurers enormous amounts to bear risk (a subject discussed elsewhere). Here’s that pie chart. Notice that TWIA policyholders now shoulder a considerably larger share of the load (about 2/3rds). There is still, however, a large chunk of the load picked up by Texas insurers/insureds (14%), coastal insureds (8%) and unfunded losses (9%). The unfunded losses are a smaller chunk because the denominator for the pie chart is now larger.

![SB 1700; Framed@Labeled[ With[{wedges = With[{t = {#[[1]], #[[2]] + #[[4]] + #[[7]], #[[3]] + #[[5]], \ #[[8]]} &[ReplacePart[Mean /@ Through[funcs[rv]], 1 -> 460000000]]}, t/Total[t]]}, PieChart[wedges, ChartLabels -> Placed[Map[ Pane[#, 144] &, {"TWIA premiums", "Texas insurers (insureds)", "Coastal insureds", "Unfunded losses"}], "RadialCallout"], ChartStyle -> Map[ColorData[61][#] &, Range[4]], ImageSize -> 580, ImagePadding -> {{110, 60}, {20, 20}}, BaseStyle -> {FontSize -> 11, FontFamily -> "Swiss"}]], Style["Distribution of expected cash payments by source", {FontSize \ -> 14, FontFamily -> "Swiss", FontWeight -> Bold}]]](http://catrisk.net/wp-content/uploads/2013/05/SB1700responsibilityBySource21.png)

Distribution of expected cash payments for 2013 under SB 1700 by source

Political Power in TRIP

TRIP will be run by a Board of Directors appointed by the Texas Governor. The graphic below shows the statutory composition of that board under new section 12 of S.B. 1700 (2210.102). Notice the little wedge representing non-seacoast interests. Hopes, therefore, that the board will take steps to protect non-coastal Texans from having their wealth transfered to the coast would thus seem very optimistic. Also notice how the southern areas of the Texas coast, which have less population and less insured property than the northern areas, have equal political power on the board. This is not a one house (or one premium dollar) / one vote system.

![Labeled[Framed@ Labeled[PieChart[{3, 1, 1, 1, 1, 1, 1}, ImageSize -> 200, ChartLegends -> Map[Pane[ Style[#, {FontSize -> 11, FontFamily -> "Swiss", LineIndent -> 0}], 216] &, {"insurance industry representatives who write \ wind/hail in first tier coastal counties", "Cameron-Kenedy-Kleberg-Willacy representative", "Aransas-Calhoun-Nueces-Refugio-San Patricio representative", "Brazoria-Chambers-Galveston-Jefferson-Matagorda-Harris \ representative", "non seacoast member", "engineer from second tier coastal county", "financial industry second tier coastal county"}], BaseStyle -> {FontSize -> 11, FontFamily -> "Swiss", LineIndent -> 0}], Map[Style[#, {FontSize -> 11, FontFamily -> "Swiss", LineIndent -> 0}] &, {"TRIP Board of Directors", "With ex-officio members: elected official from southern \ seacoast, elected official from northern seacost, elected official \ from non-seacoast"}], {Bottom, Top}], Style["Political Power in TRIP", {FontSize -> 11, FontFamily -> "Swiss", LineIndent -> 0, FontWeight -> Bold}], Top]](http://catrisk.net/wp-content/uploads/2013/05/SB1700politicalPower.png)

Board of Director membership in TRIP

The Depopulation of TWIA/TRIP

One of the concepts in SB 1700 is that TWIA/TRIP should be “depopulated” by reducing its total insured exposure (currently over $75 billion). Great. The bill does not, however, come with a magic wand with which to accomplish this task. The only tool it provides is a club that threatens the insurance industry with a collective $200 million assessment that goes into an “exposure reduction plan fund” if the 2016 target of a 20% reduction from 2013 levels is not met. It places insurers in a bit of a prisoners dilemma and creates a lot of litigation-fomenting administrative discretion on this point by saying that the assessment will only be levied against insurers that “as determined by the [TRIP] board of directors, has not met the member’s proportionate responsiiblity for reduction of the association’s total insureds exposure.” So, if all other insurers have started selling insurance — presumably at a major loss — on the coast using TWIA or sub-TWIA rates, the insurer who is left and refusing to sell insurance on the coast might find themselves with a very hefty bill even if they just have a modest share of the Texas property-casualty market. And this, I take it, is the whole point behind the clever section 2210.212 of the bill.

I suspect, however, that the $200 million assessment will be unlikely to lure many insurers back to the coast. There is going to be a first mover problem. If very few large insurers choose to avoid the 2210.212 club by selling on the coast, then no insurer ends up paying a very large 2210.212 assessment. Question for any other lawyers (or law students) reading this entry: would it violate federal antitrust laws, as modified by the McCarran Ferguson Act, for insurers collusively to refuse to sell; would it violate Texas law?

The other point — and this is the one to which the picture below relates — is that the reduction targets are ambitious. Although they are stated as reductions from the 2013 status quo, they will in fact be larger. That’s because TWIA/TRIP is likely to continue growing at significant rates. Thus, to make a 20% cut from the 2013 status quo, one needs to make perhaps a 30% cut from the 2016 expected status quo. The graph below illustrates this point by comparing 3% TWIA growth to the depopulation targets stated in section 2210.212.

![Labeled[Show[ DateListPlot[{{"January 1, 2013", 1}, {"January 1, 2016", 1.03^3}, {"January 1, 2018", 1.03^5}, {"January 1, 2020", 1.03^7}, {"January 1, 2022", 1.03^9}, {"January 1,2024", 1.03^11}}, PlotRange -> {0, 1.4}, PlotMarkers -> Automatic, PlotStyle -> Green, FrameLabel -> {"Time", "Total Insured Exposure As Fraction of 2013"}, BaseStyle -> {FontSize -> 11, FontFamily -> "Swiss"}, Epilog -> {Arrow[{{3.6238320000000005*^9, 0.28615669133896926}, {3.6578745686249995*^9, 0.7181793832820529}}], Inset[TextCell["Assessment of $200\nmillion if not reached", GeneratedCell -> False, CellAutoOverwrite -> False, CellBaseline -> Baseline, TextAlignment -> Left], {3.588546672*^9, 0.19378500614472127}, {Left, Baseline}, Alignment -> {Left, Top}]}], DateListPlot[{{"January 1, 2013", 1}, {"January 1, 2016", 0.8}, {"January 1, 2018", 0.65}, {"January 1, 2020", 0.55}, {"January 1, 2022", 0.45}, {"January 1,2024", 0.4}}, PlotMarkers -> Automatic, PlotStyle -> Red]], Style["Natural Growth of TWIA/TRIP (green) compared to 2210.212 \ \"requirements\" (red)", {FontSize -> 11, FontFamily -> "Swiss"}] ]](http://catrisk.net/wp-content/uploads/2013/05/SB1700DepopulationPlot.png)

Natural growth of TWIA/TRIP compared to 2210.212 requirements

My final picture is of Albus Dumbledore and the most powerful wand in the universe: the Elder Wand. I show it because, I suspect, that is what it is going to take for TRIP to actually accomplish the targets set forth in the legislation without infuriating the very political constituencies that have, with SB 1700, again kicked the fundamental problems of catastrophic risk transfer down the road.

Perhaps the only thing that will actually be able to implement the SB 1700 targets without infuriating coastal Texans

TRIP could raise premiums drastically to market rates. That would likely reduce total insured exposure, but somehow I don’t think that is the idea in the legislation. It could refuse to take on new customers. Imagine the squeals that will produce. It could do what I have suggested for years and refuse to insure beyond some basic amount and rely on market-provided excess insurance for the rest. To do so to the extent of the targets contained in SB 1700 will likely require that excess policies kick in at about $100,000. Again, I have doubts that his what the proponents of this legislation have in mind. Or, finally, TRIP could just realize that its impossible to reduce total insured exposure without taking steps that are going to be extremely unpopular with the very constituencies that put forth this bill. They could, instead, giggle. They could recognize that the “must” language in the bill is basically a legislative joke — a pretext for extracting in disguise another $200 million out of Texas insureds throughout the state to subsidize, yet again, coastal property, owned by poor and wealthy alike.