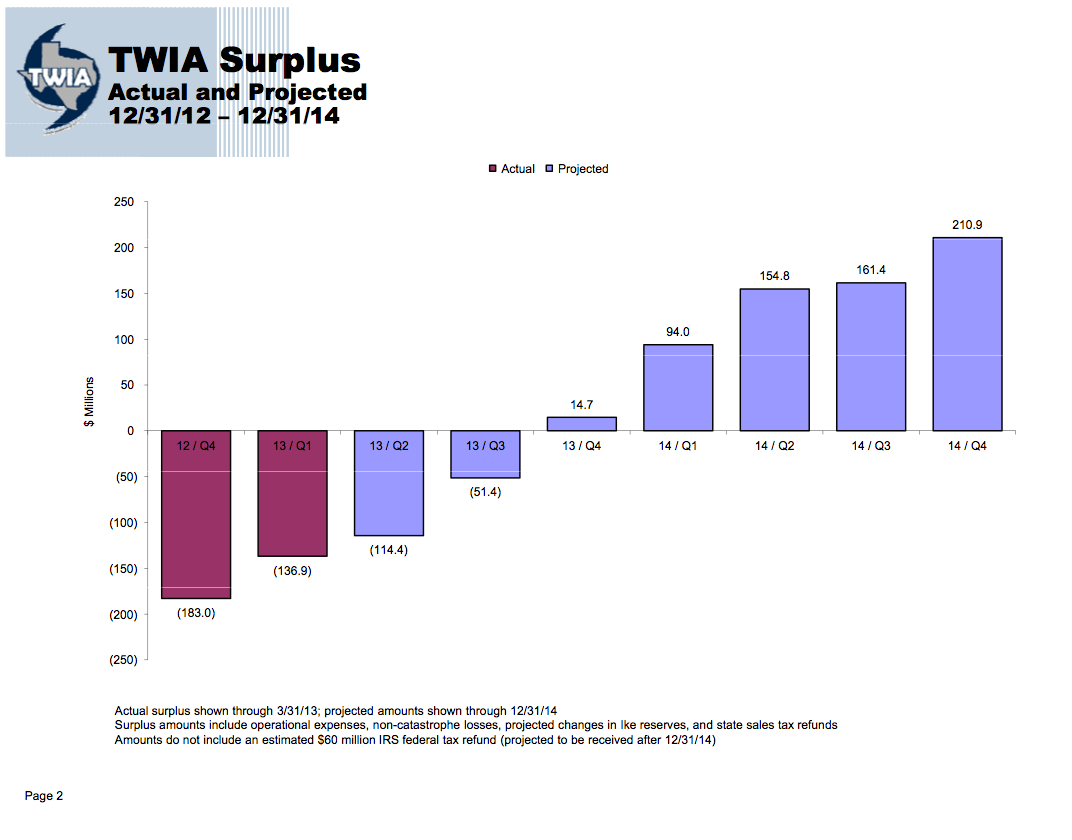

Associated Press reports are successfully repeating the message the Texas Windstorm Insurance Association leadership sought to convey at today’s special meeting of the House Insurance Committee: “Coastal Group Expects Surplus” is the headline, for example, that the Houston Chronicle attaches to the AP report. Unfortunately for TWIA policyholders or any legislators misled by today’s presentation, the surplus scenario is essentially a picture of the best possible world in which no significant storms affect the largest windstorm insurer on the Texas coast. Thus, while the graphic is not false, all it really does is confirm that insurance companies, even ones with premiums that do not reflect risk, make money if they never have any large claims. It is not, however, an accurate depiction of reality.

Here’s the happy picture that TWIA wants the world to see. Surplus goes in a predictable linear way from that troublesome negative (red) $183 million in the fourth quarter of 2012 to a cheerier (blue) positive $211 million by the fourth quarter of 2014. That’s the picture presented by TWIA lawyer David Durden, TWIA chief actuary James Murphy and Pete Gise, TWIA’s comptroller at yesterday’s special meeting of the House Insurance Committee. It is a picture that will make unquestioning TWIA policyholders breathe a sigh of relief, lessen pressure to reform TWIA, forestall efforts to place the insolvent insurer into receivership and let those who profit from the band playing on continue to do so for a time.

A misleading projection of TWIA finances

But look carefully at the fine print in the foonotes for this graphic. “Surplus amounts include operational expenses, non-catastrophe losses, projected changes in Ike reserves, and state sales tax refunds.” What’s not included? TWIA doesn’t say in the graphic, but I can tell you. What TWIA does not include is the main thing TWIA was set up to handle and for which it needs catastrophe reserves: large losses from tropical cyclones. (I’m also not sure they are taking account of reinsurance premiums, which now consume more than 20% of TWIA premiums). In other words, TWIA could have shown roughly the same “projected” increase in surplus in any year it chose, ranging from the year before Hurricane Ike to the year before Hurricane Alicia. And TWIA would have been equally misleading in doing so.

And what is the probability that over the next two hurricane seasons TWIA will incur no tropical cyclone expenses. Assuming we have normal hurricane seasons over the next two years– which itself is rather optimistic given the unanimous forecasts of weather experts — the probability is about 1/3. Even with the most optimistic estimates of Texas hurricane frequency, the probability that the TWIA graph accurately projects reality is less than half. So, yes, less than half the time, the graphic produced by TWIA might be accurate.

The majority of the time, however, the TWIA graphic will be wrong. And some of the time it will be seriously wrong. This is exactly why every actuary who has consulted for TWIA or TDI in recent times has noted that TWIA takes in too little revenue relative to expenses to sustain a surplus. On average, in any two year period during which TWIA suffers a significant loss (i.e. a loss greater than $50 million), the average total loss during that time period is well over $500 million. Such losses would in fact significantly increase the deficit TWIA now suffers from. This is based on the Compound Poisson Distribution discussed on this blog as a way of modeling annual losses to TWIA and emulating the sophisticated work of state-of-the-art storm modelers such as AIR and RMS. The Mathematica code proving this point is shown at the bottom of this post.

When we actually take possible storm losses into account, the two year position of TWIA is likely to be worse or no better than it is today.

I’ve tried in this blog to stay away from accusations of bad faith. People have honest disagreements and different values. And I have had respect for people doing what must be difficult work at an insurer with little money. And this graphic did, after all, have a footnote from which one knowledgable in the area might recognize that the graphic was missing critical information. And TWIA did disclose at the hearing — after a lengthy exposition of the graphic — that their graphic assumes no storm losses. But to me it is like presenting a graphic projecting how well the Astros are likely to do this year based on how they do during their best periods without taking into account the fact that they also suffer a lot of losing streaks. It is, at best, an insulting partial truth, one that I hope reporters, legislators and, tomorrow, the TWIA Board of Directors, are smart enough to see through.

The code

Mean[Total /@Map[Max[# – 50000000, 0] &,

DeleteCases[Partition[RandomVariate[CompoundPoissonDistribution[0.54,WeibullDistribution[0.42, 177000000]], 10000], 2, 1], {0,

0}], {2}]]