At yesterday’s hearing of the House Insurance Committee, leadership of the Texas Windstorm Insurance Agency presented a packet of three graphics to the members. These graphics joined a crucial presentation created for today’s meeting of TWIA’s board of directors that falsely identified how post-event bonds would be paid off under existing law. Together, it presents a picture of an insurer less interested in forthrightly informing legislators than in trying to preserve its troubled existence.

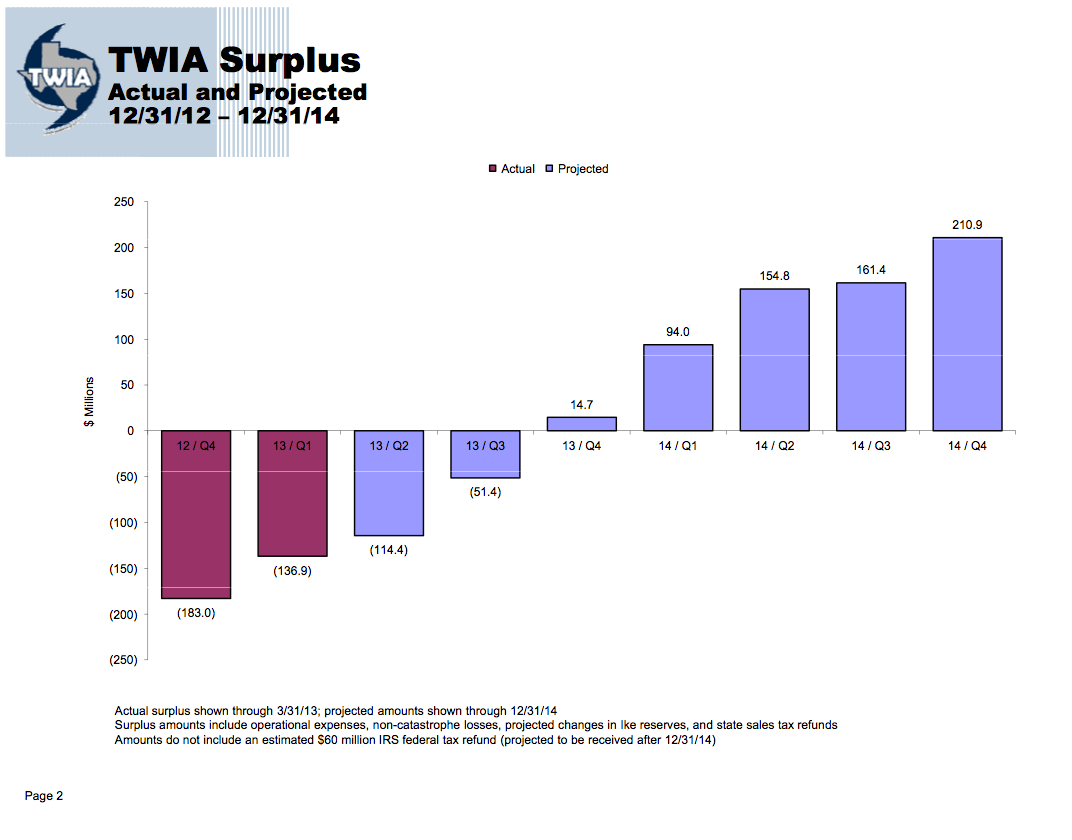

As discussed in blog entries yesterday, the first two of the graphics presented yesterday to the House Insurance Committee were highly confusing if not downright misleading. The first graphic, which purported to project TWIA going from insolvent to a positive surplus position over the next two years simply assumed away the possibility of any large claims being made against TWIA. What insurer can’t improve its position when no large claims are filed? There would be little need for solvency regulation if insurers never incurred large claims.

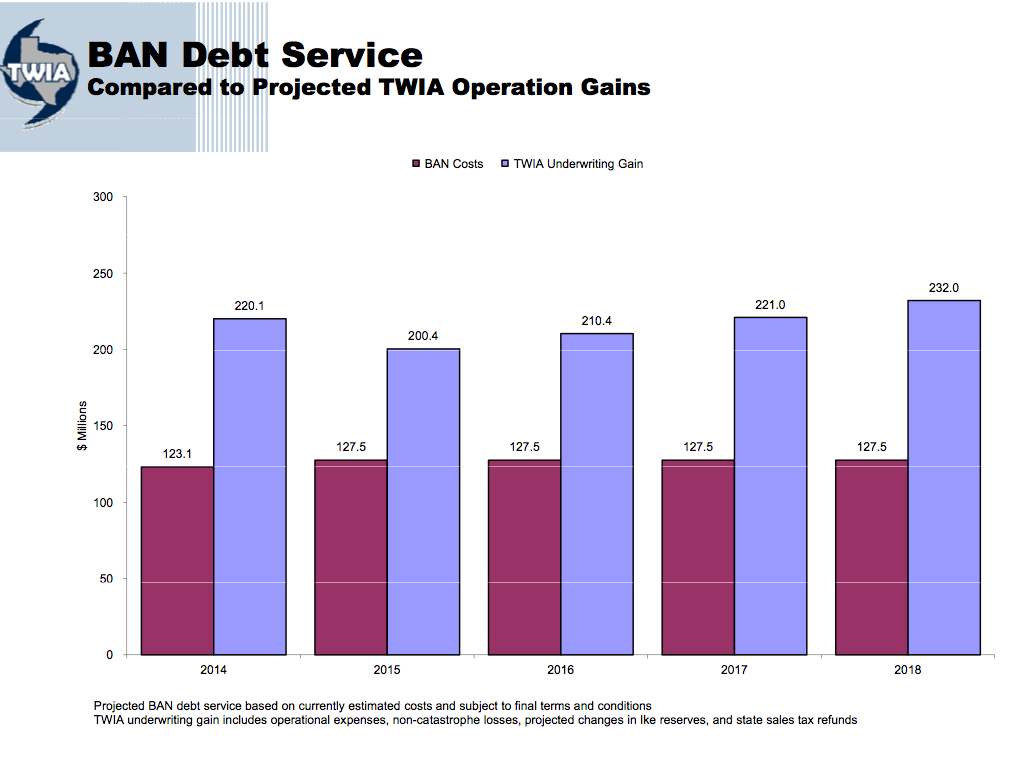

The second graphic presented yesterday purported to show that TWIA could pay off the borrowing of $500 million it wants to make in that its underwriting profit was greater than its debt service. Again, however, TWIA simply assumed that it would not have any large claims that would deplete its profit. Lots of people who borrow too much on their credit cards might have been able to pay them off it nothing else had happened. Problem is, stuff happens. And then, the borrower can’t pay.

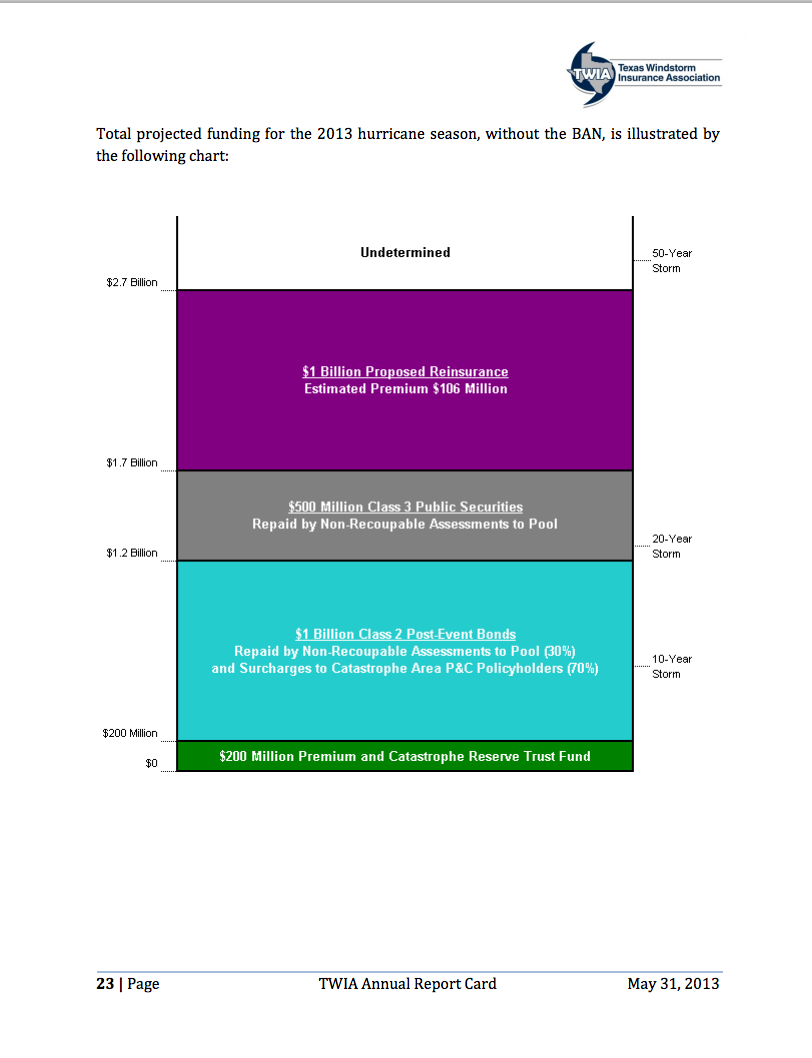

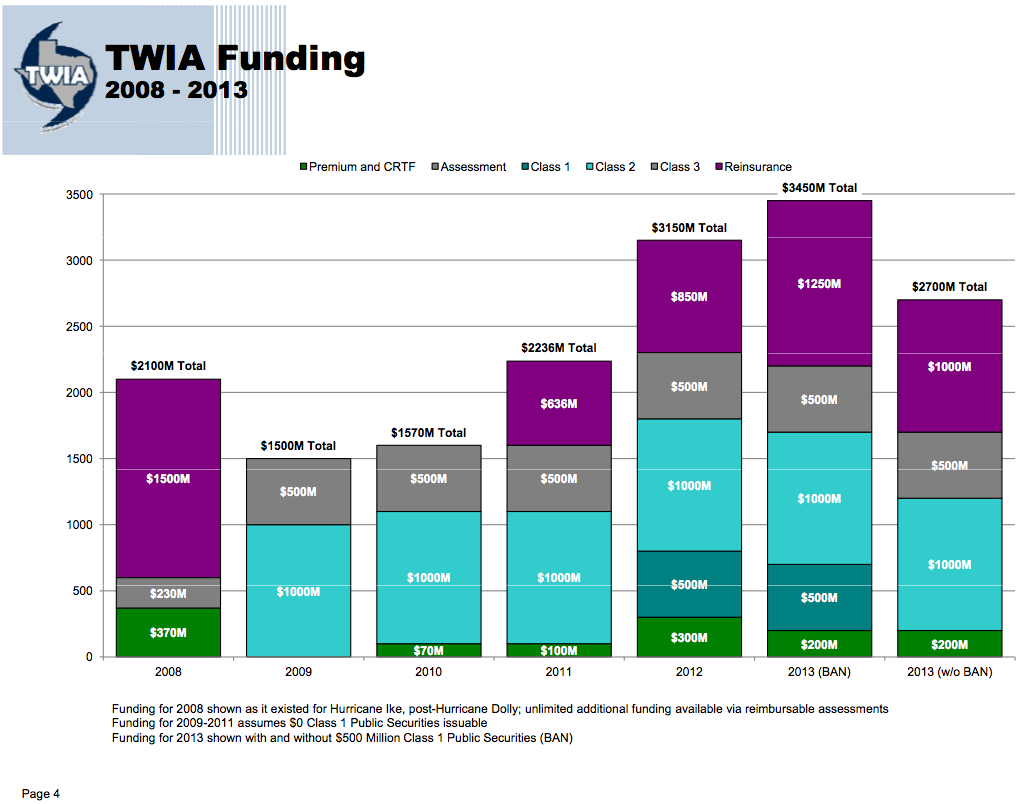

Today, I want to tackle the third graphic submitted to the House Insurance Committee by TWIA. It appears to continue what may be a pattern of misleading visual information. Here’s the picture.

TWIA’s stack size with misleading information on 2008 and failure to adjust for exposure

Let’s look at that left hand bar, the one for 2008. It would appear to show that TWIA had only a $2.1 billion stack for that year. I believe legislators were supposed to gain comfort from the fact that the stack for 2013, with or without $500 million in pre-event borrowings known as a BAN (bond anticipation note) is actually higher than that amount.

But the stack appeared to be only $2.1 billion for 2008 because TWIA staff had simply not counted the leading source of protection for TWIA that existed at that time. TWIA’s graph simply deleted the key fact: TWIA had the ability to make unlimited assessments against the insurance industry. TWIA thus had essentially a 100% guaranty of being able to pay claims. A proper picture would have had another gray bar extending high above the purple one showing this ability to assess. The gray bar would be just like the $230 million one it made lower in the stack. It would be just like the one I am confident TWIA would have stuck over the 2013 stack if such an ability existed today. I can think of absolutely no good reason why this bar should have been eliminated from the graphic.

Now, it is true that TWIA disclosed in a fine print footnote to the graphic “unlimited additional funding available via reimbursable assessments.” Do you see it? Look after the semi-colon in the first line at the bottom. But, again, that’s relegating the central point to a footnote and leaving the big graphic in a highly misleading condition.

I’ve got two other problems, by the way, with the graphic.

Stack size is best measured relative to exposure

Comparisons of stack size can be misleading without taking exposure into consideration. A stack of $2.7 billion might be just fine if TWIA had exposure of $20 billion whereas a bigger stack of $3.5 billion might be inadequate if TWIA had exposure of $80 billion. Once we do this, the picture becomes a little less cheery. In 2008, for example, when TWIA’s stack was essentially unlimited, TWIA direct exposure was $64 billion. Today, it is about $75 billion. To have a $2.1 billion stack in 2008, is roughly the same as having a $2.46 billion stack today.

There is no apparent reason to have ignored Hurricane Dolly payments

I do not understand why TWIA excluded money paid for Hurricane Dolly from the 2008 stack. That would have made it a little higher. I suppose the purpose was to contrast preparedness for Ike with preparedness for today’s storms. Again, though, that seems a peculiar choice. In assessing TWIA’s ability to pay claims, a more relevant comparator is stack size at the start of hurricane season. Had TWIA done this properly the stack in 2008 — the year of Ike — would have been much higher even without consideration of TWIA’s ability at the time to make unlimited assessments.