State Senator Juan “Chuy” Hinojosa (D-McAllen) and State Representative Todd Hunter (R-Corpus Christi) have filed companion bills in the State Senate (SB 1089) and State House (HB 2352) that would buttress the resources available to the Texas Windstorm Insurance Association (TWIA) to pay claims in the event of a tropical cyclone hitting the Texas coast but would do so by placing most of the burden either directly or indirectly on policyholders living away from the Texas coast. The bill, like the current system and as heralded in recommendations of the Coastal Windstorm Task Force, would rely primarily on post-event bonding as a way of financing catastrophic risk. But, by impelling insurers statewide and coastal policyholders to increase the size of the catastrophe reserve that pays before any bonds are issued, the bill would make it less likely that this system of “insurance in reverse” would need to be used. The new system would come into effect in September of 2013. It would apparently leave the current system in place for much of this hurricane season.

In a nutshell, here’s how the Hinojosa/Hunter plan works. TWIA builds up its catastrophe reserve trust fund (a/k/a CRTF, a/k/a “cat fund”) so that it equals 1.5% of its “direct exposure” for the prior year. (Section 2210.456). Since TWIA lists its current direct exposure at $72 billion, this means the catastrophe reserve fund is supposed to grow to at least $1.08 billion. Catrisk’s earlier modeling suggests that such a catastrophe reserve fund would be able to cover something like a 1 in 20 year storm.

But just because TWIA’s catastrophe reserve fund could cover a 1 in 20 year storm, does not mean that TWIA’s policyholders would be paying to cover that risk. That’s because under the Hinojosa/Hunter plan, the catastrophe fund is financed mostly with other money. To get from the paltry $180 million that now stands in the fund to $1.08 billion, the plan would assess property insurers statewide, regardless of the extent to which they choose to do business on the Texas coast, 1/10 of the desired amount of the catastrophe reserve fund each year. (Section 2210.456(c) (0.15% of the direct exposure)). As it stands, this would amount to $108 million per year for many years into the future. These are real assessments, not compelled loans by the insurance industry. The assessments are not creditable against premium taxes otherwise owed and are not supposed to be passed on — at least directly — by a premium surcharge on policyholders. It would demean the insurance industry, however, to suggest that they will not be clever enough to find a way to pass much of this cost on to policyholders.

Coastal insureds — including non-TWIA homeowner insureds and coastal residents with automobile insurance or other forms of property insurance — also pay to protect TWIA policyholders from risk. Under the Hinojosa/Hunter plan, a 3.9% premium surcharge is issued on all such policies. How much would this surcharge bring in? Unclear. I don’t have the data, yet, particularly on automobile policies along the coast. But we do know how much TWIA policyholders would pay on their TWIA policies to increase the protection available to them: about $17 million (0.039 x $446 million in premium taxes). And since TWIA reports that it 62% of the coastal homeowner wind market (measured by exposure and not premiums), one can approximate that non-TWIA homeowner insureds would pay roughly $11 million. Thus, TWIA policyholders would, at most, pay about 13% of the amount it will take to strengthen the catastrophe reserve fund that would be exclusively available to those policyholders to pay claims in the event of a tropical cyclone. If, as I suspect, non-wind homeowner policies, automobile policy premiums and other property insurance premiums along the coast are at least as large as TWIA premiums, the surcharge on TWIA policies will, at least for a few years, in fact pay perhaps just 7% of the actual cost of this portion of the risk posed by such policies.

And even this last figure of somewhere between 7 and 13% potentially understates the degree to which TWIA policies will be funding the risk they pose. This is because under section 2210.083 of the Hinojosa/Hunter bill, when the cat fund needs to be restocked following a disaster that wipes it out, insurers doing business anywhere in the state must promptly pay, in addition to the regular shortfall assessment and in addition to whatever else they may be paying their own policyholders, half the amount of any public securities (up to $1 billion) issued to pay TWIA policy losses and, as I read section 2210.084, the entirety (up to $900 million) of additional public securities issued to pay TWIA losses. Thus, following a serious hurricane, even more of the money used to pay for future hurricane losses will be coming from sources other than TWIA policies. Of course, the Hinojosa/Hunter bill permits insurers to “reinsure” against these potential assessments (section 2210.088), but this just means that insurers will be paying cash for the risk imposed on them by the law rather than perhaps just making an accounting entry for contingent liabilities on their books.

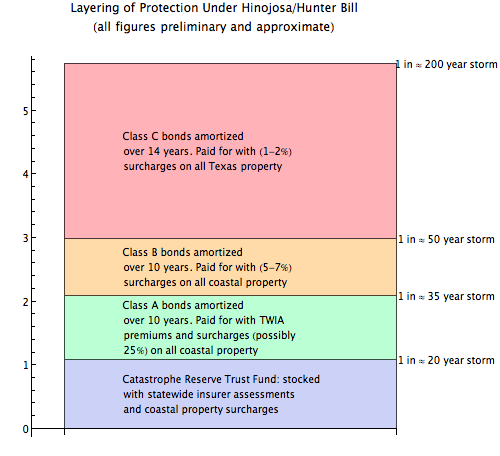

Layering of Protections Under Hinojosa/Hunter Bill

The Hinojosa/Hunter provides for at least three heightened layers of protection in the event of a storm that pierces the catastrophe reserve fund. Each of the layers is provided by bonds, issued after the disaster, by the Texas Public Finance Authority. The layers (Classes A, B and C) differ primarily in their amortization periods and in the source of money used to repay the debts. Up to the first $1 billion is to be provided by Class A securities with an amortization period of 10 years. The money to repay this debt each year — probably about 1/8 of the amount borrowed — will come from TWIA itself. If the full $1 billion were borrowed, this would likely amount to a charge of $125 million per year for 10 years, which in turn would increase existing TWIA premiums by 25%. It is not clear whether the market would trust the ability of TWIA to actually obtain these funds, since some TWIA policyholders might be reluctant to renew with TWIA in the event such a hefty increase were imposed. The Texas Public Finance Authority has published grave doubts about the ability to market similar bonds authorized by the current law.

Class B bonds can be issued in an amount up to $900 million and likewise must be amortized in no more than 10 years. The source of repayment, though, is different. Although TWIA premiums could in theory be used to repay this obligation — I rather suspect they will be tied up elsewhere — the vast bulk of the funding is likely to come from yet another surcharge: this one on all premiums on coastal property insurance, including non-TWIA wind insurance, conventional coastal homeowner insurance, automobile insurance, and other forms of property insurance. The surcharge won’t be another 25% because the base is bigger. But since it will cost $110 billion or more each year to amortize the debt, I would not be surprised to see an additional 5 to 7% surcharge.

If the catastrophe reserve fund indeed bulks up to $1.08 billion and the Class A bonds are indeed marketable, the Class B bonds should cover TWIA against the 1 in 50 year storm. For storms bigger than that, the Hinojosa/Hunter bill provides for $2.75 billion in Class C bonds. These have an amortization period of 14 years. They are to be paid by a surcharge on all premiums on property insurance statewide. The rate will be about 1/10 of the amount borrowed divided by a denominator that I would love to know the value of: the amount of premiums on property insurance sold in this state. If you forced me to make an educated guess, however, I would guess that property insurance premiums in Texas are about $20 billion per year, which would put the needed surcharge at 1-2% per year for 14 years. Of course, if the amount borrowed were not the full $2.75 billion, the surcharge would be less.

There are two other sources of funds worth mentioning. The Hinojosa/Hunter plan continues to permit TWIA to purchase reinsurance and imposes no price constraints upon their doing so. Such reinsurance is notoriously expensive and often difficult to obtain. There is no explicit provision or encouragement for other forms of protection such as pre-event catastrophe bonds. There are also, in theory, Class D securities that provide an unlimited amount of protection to TWIA policyholders. The problem: no source of funds is identified to pay back the bonds. Section 2210.639 simply mentions that these borrowings could be paid by TWIA premiums (yeah, right) or “money received from any source for the purpose of repaying Class D public securities.” In other words, no one has a clue.

There is more in the Hunter bills and the Hinojosa bill that Catrisk will try to address in the near future. And there are some simulations we can run to get some better ideas of the relative burdens borne throughout Texas under this bill. But this should provide an explanation of the basics.

Footnote: I bet that I am going to hear the double dipping criticism of this post again. The point of these critics is that TWIA policyholders also have conventional homeowner insurance and automobile insurance. Thus, their burden is higher than I have reported because they get hit with a double or triple whammy. There is some truth to this criticism. My defenses are (a) I have tried to report data here as policy based rather than policyholder based; thus the conclusions reached here should be accurate; (b) I can;t find and no one has volunteered the data needed to make the needed computational adjustments; if I had them I could and would do so. My suspicion is that, while a few numbers would change, the themes of the Hinojosa/Hunter bills would not. They believe coastal risk should be socialized and these bills very much reflects that philosophy.